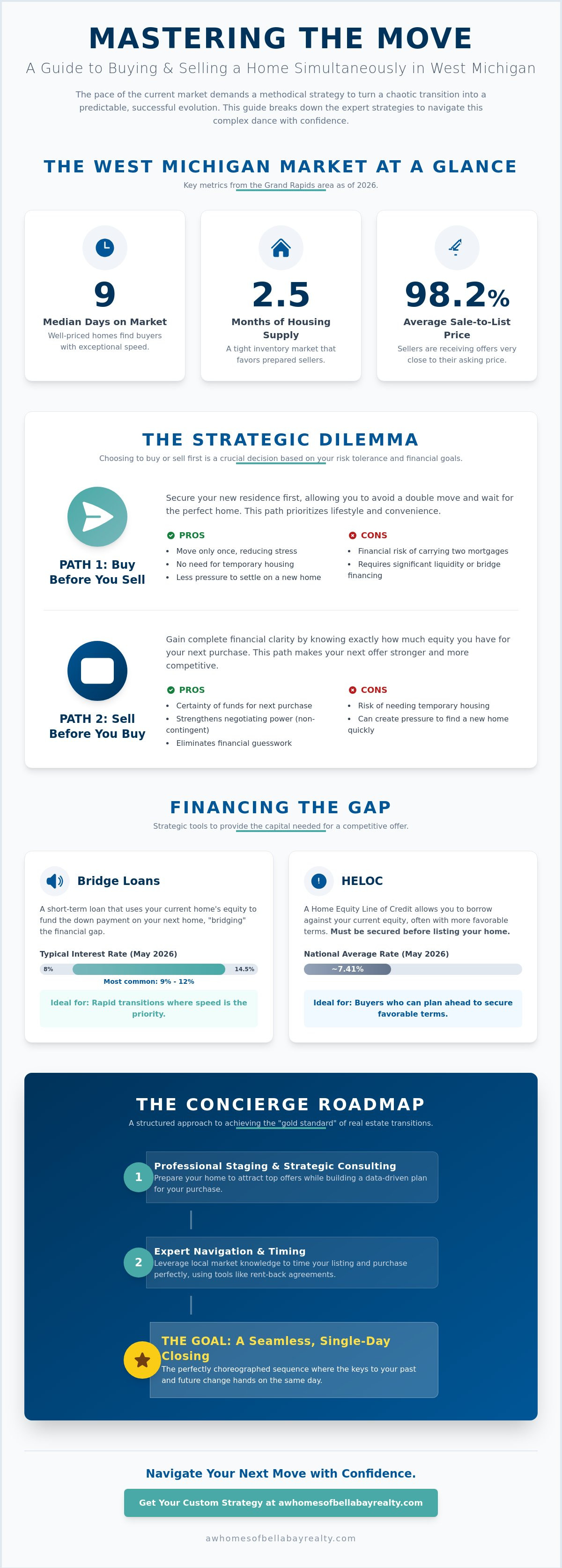

The idea of selling and buying a house at the same time often feels like trying to land a plane on a moving ship. You worry about the "gap" period where you have nowhere to go, or worse, the financial strain of carrying two mortgages at once. With the median days on market in Grand Rapids sitting at just nine days as of April 2026, the pace of the current market demands more than just luck. It requires a methodical strategy that turns a chaotic transition into a predictable, successful evolution for your family.

You likely feel that the stakes are too high to leave anything to chance, and you're right. This guide will show you how to master the complex dance of simultaneous transactions by using expert strategies tailored specifically for the West Michigan market. We will explore how to unlock your equity for a competitive down payment, manage all moving parts with precision, and achieve a seamless, single-day closing. From leveraging bridge loans to timing your residential listing perfectly, you'll learn to navigate this transition with total emotional security and professional confidence.

Key Takeaways

- Analyze your unique risk tolerance to determine whether a "sell first" or "buy first" strategy provides the most financial certainty for your transition.

- Explore how strategic financing tools like bridge loans and HELOCs provide the capital needed for a competitive offer before your current equity is unlocked.

- Learn to time your move around West Michigan’s seasonal inventory shifts in areas like Ada and Forest Hills to ensure you find your next home.

- Master the complex process of selling and buying a house at the same time through the expert use of Hubbard clauses and strategic rent-back agreements.

- Follow a structured concierge roadmap that integrates professional staging, strategic consulting, and expert navigation for a seamless, single-day closing.

The Strategic Dilemma: Should You Buy or Sell First in 2026?

Choosing between purchasing your next property or listing your current one first is more than a logistical hurdle; it's a profound decision about your family's future. This choice requires you to balance financial safety, lifestyle convenience, and emotional security. In the current West Michigan market, where inventory remains tight at approximately 2.5 months of supply, the stakes of selling and buying a house at the same time have never been higher. You aren't just moving furniture; you're evolving your life story.

Your risk tolerance serves as the primary compass for this journey. Some homeowners prioritize the absolute certainty of funds, while others value the ability to secure a dream home in Forest Hills or Ada without the pressure of a ticking clock. Understanding the process of a real estate transaction is essential to making an informed choice that protects your equity. In 2026, well-priced homes in Grand Rapids are finding buyers in a median of just nine days. This velocity means you must have a plan that accounts for speed, precision, and local leverage.

Option A: Buying Your Next Chapter Before Selling the Current One

This path is often the preferred choice for those with high liquidity or verified access to bridge financing. By securing your new residence first, you avoid the exhaustion of a double move and the unnecessary costs of temporary rentals. It allows you to wait for the perfect home to appear on the market without compromise. However, this strategy carries the weight of two mortgages if your current property doesn't sell as quickly as anticipated. It's a move defined by lifestyle first, financial flexibility second, and strategic patience third.

Option B: Selling Your Current Home to Unlock Maximum Equity

Selling first provides a level of financial clarity that many find deeply reassuring. You'll know exactly how much equity you have for your next down payment, which eliminates guesswork and strengthens your negotiating power. In a market where sellers are receiving an average of 98.2% of their asking price, being a non-contingent buyer makes your offer stand out. The challenge here is logistical. You may need to manage temporary housing or negotiate a post-closing occupancy agreement to bridge the gap between your old life and your new one.

While both paths have merit, the simultaneous close remains the gold standard for move-up buyers. It represents a perfectly choreographed sequence where the keys to your past and the keys to your future change hands on the same day. Achieving this requires a methodical approach that aligns your financial goals with the unique rhythm of the West Michigan market, ensuring no detail is left to chance.

Financing the Gap: Strategic Tools for a Seamless Transition

The financial logistics of selling and buying a house at the same time often feel like the most daunting part of the journey. However, with the right capital strategy, you can move with confidence and clarity. Financing isn't merely about debt; it's a tactical instrument that allows you to bridge the gap between your current equity and your future home. By identifying the right tool, securing your capital, and executing your move with precision, you can avoid the financial strain of two mortgages.

Bridge loans are a primary solution for move-up buyers in West Michigan. These short-term loans provide the liquidity needed for a down payment on your next property before your current home is sold. In May 2026, bridge loan interest rates typically range from 8% to 14.5%, with most borrowers finding options between 9% and 12%. While the rates are higher than a traditional mortgage, the value lies in the speed, flexibility, and emotional security they provide during a high-stakes transition.

A Home Equity Line of Credit (HELOC) offers another tactical path. With national average rates around 7.41% as of late May 2026, a HELOC allows you to tap into your existing home's equity with more favorable terms than a bridge loan. The critical requirement is timing. You must secure this line of credit while your current residence is not yet listed on the market. This tool provides a safety net of funds that you can use for a competitive down payment or to cover closing costs during the transition.

Bridge Loans vs. HELOCs: Which Fits Your Transition?

Choosing the right tool depends on your specific liquidity needs and timeline. Bridge loans are ideal for rapid transitions where speed is the priority. HELOCs are better suited for homeowners who plan their move months in advance and want to minimize interest expenses. When you compare the total cost of interest against the logistical expense of a double move, professional storage, and temporary housing, these strategic financing tools often prove to be the more economical choice.

The Power of the Cash-Back Offer

In a competitive market like Grand Rapids or Forest Hills, making an offer that is "as good as cash" can be your greatest leverage. By using a bridge loan or HELOC to remove the sale-of-home contingency, you position yourself as a high-level buyer. This strategy requires a deep understanding of the Michigan home closing process to ensure all dates align perfectly.

For those looking to lower their long-term costs, the "recasting" strategy is an excellent post-closing tool. Once your old home sells, you can apply a large lump sum to your new mortgage, and many lenders will re-calculate your monthly payment based on the new, lower balance. For personalized guidance on which tool fits your equity position, speaking with a strategic advisor can help clarify your options and protect your long-term well-being.

Navigating the West Michigan Market: Local Timing and Inventory

The West Michigan landscape is not a monolith. Success in selling and buying a house at the same time depends entirely on your ability to read the specific micro-markets of our region. While national headlines may suggest a cooling market, the reality in Forest Hills, Ada, and East Grand Rapids remains one of focused competition. As of April 2026, our regional housing inventory sits at approximately 2.5 months of supply. This is well below the five to six months required for a balanced market. Understanding these Grand Rapids real estate trends allows you to predict your "Days on Market" with professional precision rather than guesswork.

Timing your transaction requires an understanding of the local "Spring Surge" and "Autumn Calm." In communities like Caledonia and Cascade, the market rhythm is dictated by school district cycles. Families often begin their search in late March to ensure they're settled before the new academic year. This surge in buyer demand creates the perfect environment to list your current home, yet it also increases the competition for your next purchase. Conversely, the autumn months offer a more contemplative pace, providing move-up buyers with slightly more breathing room to negotiate terms without the frenzy of multiple-offer scenarios.

Inventory Realities in Forest Hills and Ada

Move-up buyers in Forest Hills and Ada face a unique challenge: the scarcity of luxury listings. While new construction is slowly adding to the total inventory, existing home values remain resilient because of the established neighborhood charm and mature landscapes. Finding your next chapter in these districts often requires looking beyond public listings. A deep local network can reveal off-market opportunities, allowing you to secure a property before it ever hits the open market. This proactive approach mitigates the fear of missing out on a dream home while your current residence is still being prepared for sale.

Leveraging Local Demand to Dictate Your Terms

High demand in areas like East Grand Rapids provides you with significant leverage as a seller. When you have multiple parties interested in your property, you can negotiate terms that facilitate a smoother transition, such as a free rent-back period or a delayed closing date. Setting a strategic "Offer Review" date is a methodical way to group interest and choose the buyer whose timeline best aligns with your own purchase. For those preparing to list, following a specialized sell my home Forest Hills MI strategy ensures your property is positioned as the premier choice in the market, granting you the leverage needed to manage both transactions with total emotional security.

By identifying your micro-market, timing your listing to school cycles, and leveraging local demand, you move from a position of chance to one of expert navigation. This strategic focus ensures that your evolution from one home to the next is as seamless as possible.

Mastering the Art of the Real Estate Contingency and Rent-Back

Navigating the legal intricacies of selling and buying a house at the same time requires a sophisticated blend of protection, flexibility, and professional foresight. You aren't just signing documents; you're building a bridge between two significant life chapters. The "Subject to Sale" contingency serves as your primary shield, ensuring your earnest money deposit remains protected if your current residence fails to close. While some generalist platforms suggest contingencies are a weakness, a methodically structured offer provides the clarity needed to move forward with confidence.

In high-velocity markets, a "Hubbard Clause" offers a tactical compromise. This clause allows you to enter a contract on your new home while keeping your current property active on the market. If another buyer emerges for your next house, you typically have a brief window to remove your contingency or step aside. This keeps the transaction moving toward a successful outcome without locking either party into an indefinite wait. It is an organized, logical way to manage the inherent risks of a dual transaction.

The "Rent-Back" Strategy: A Bridge to Your New Home

A rent-back agreement, or post-closing occupancy, is often the key to a single, stress-free moving day. In Michigan, these agreements must be precisely structured to meet legal standards, defining daily occupancy rates and security deposits. Staying in your home for 30 to 60 days after closing allows you to finalize your purchase and move directly into your next residence. This approach is frequently more economical than a temporary hotel stay and significantly less taxing than a double move. It provides the emotional security you need to focus on your family's evolution.

Making Your Contingent Offer Irresistible

To stand out among non-contingent buyers, you must present a "clean" listing that is ready for an immediate sale. This involves completing a home inspection and professional staging before you even make an offer on your next property. By shortening the "Sale of Home" deadline, you reassure the seller that your timeline is aggressive and realistic. Leveraging a concierge real estate service MI helps you pitch your offer with professional authority, showing the seller that every detail of your dual transaction is being managed by a transition specialist.

Every detail of your move should be handled with intentionality and expert insight. To begin crafting your own customized transition plan and ensuring your offer is the one that gets accepted, schedule a strategic consultation today. This methodical preparation moves you away from chance and toward a successful, single-day closing.

The Concierge Roadmap: A Seamless Transition with AW Homes

Mastering the process of selling and buying a house at the same time requires more than just luck; it demands a choreographed roadmap designed to protect your long-term well-being. At AW Homes, we view this transition as a significant personal milestone rather than a mere financial transaction. Our concierge approach moves beyond simple salesmanship to position us as your high-level consultant through five essential stages. We analyze, align, and act with a methodical focus that ensures no detail is left to chance.

- Step 1: The Strategic Consultation. We begin by aligning your financial and lifestyle goals to create a personalized blueprint for your move.

- Step 2: Market Preparation. Our residential listing services include professional staging and high-end photography to ensure your home commands maximum attention.

- Step 3: The Search. We leverage deep local insights to find your next West Michigan residence, often identifying opportunities before they hit the open market.

- Step 4: The Choreography. We manage the transaction pipeline, aligning closing dates and overseeing the complex paperwork of simultaneous closings.

- Step 5: The Handover. We ensure a smooth move by coordinating with vetted local partners, allowing you to step into your next chapter with confidence.

Orchestrating the Timeline: From Listing to Keys

The inherent stress of high-stakes transactions is often rooted in the fear of the unknown. We mitigate this by providing a single point of contact for both your sale and your purchase. This unified approach prevents the communication gaps that often lead to delays. By managing the transaction pipeline with professional authority and empathetic reassurance, we provide the emotional security you need. Our goal is a transition that feels steady, logical, and supportive from the first consultation to the final signature.

Reducing the Logistical Burden of Your Move

A successful evolution to a new home involves more than just a deed transfer; it requires managing the physical reality of the move. We offer relocation assistance that connects you with vetted West Michigan movers, cleaners, and organizers. This allows you to focus on your family while we handle the "move-in" prep for your new residence. Whether you are moving across town or across the county, our Grand Rapids relocation guide provides the strategic roadmap you need for a stress-free experience. Experience your next chapter with a partner who understands that every detail matters in the pursuit of a seamless transition.

Step Into Your Next Chapter with Confidence

The journey of moving from one home to the next is a significant personal milestone that defines your family's future. You've learned how strategic financing, micro-market timing, and expert contingencies turn a complex transition into a predictable success. By prioritizing your financial safety, lifestyle goals, and emotional security, you can master the art of selling and buying a house at the same time without the stress of the unknown. Your evolution as a homeowner should be marked by clarity and intentionality.

As specialized experts in the Forest Hills and Ada micro-markets, we provide the concierge-level transaction management required for high-stakes moves. We focus exclusively on move-up buyer transitions, ensuring that every detail of your evolution is handled with precision, authority, and care. From professional staging to aligning simultaneous closings, our methodical approach removes the logistical burden from your shoulders. You deserve a partner who values your long-term well-being over a quick closing.

You don't have to navigate this transition alone. To begin your unhurried journey toward a single-day closing, Schedule Your Strategic Transition Consultation with AW Homes today. Your future is waiting, and it's time to move forward with total peace of mind.

Strategic Answers for Your Transition

Can I use the equity from my current home for a down payment before it sells?

You can access your equity through strategic financial instruments like bridge loans or a Home Equity Line of Credit (HELOC). These tools allow you to make a competitive offer on your next property before your current residence is officially sold. Bridge loans typically carry rates between 9% and 12% as of May 2026. This tactical approach ensures you have the liquidity needed for a down payment while maintaining your emotional security.

What is a 'sale of home' contingency and how does it work in Michigan?

A "sale of home" contingency is a protective clause that makes your purchase offer dependent on the successful closing of your current property. In Michigan, this often involves a Hubbard Clause, which allows the seller to keep their home on the market while you work toward a sale. It acts as a vital safety net for your earnest money deposit. This methodical structure ensures your transition remains organized and logical.

Is it better to buy or sell first in a competitive market like Grand Rapids?

In a high-velocity market like Grand Rapids, where the median days on market was just nine days in April 2026, selling first often provides the most negotiating leverage. This strategy eliminates the need for a home-sale contingency, making your offer far more attractive to sellers. However, those with high liquidity may choose to buy first to secure a rare luxury listing in Forest Hills or Ada without the pressure of a deadline.

How long does a typical simultaneous closing take from start to finish?

A typical simultaneous transaction usually spans 30 to 60 days from the initial contract to the final handover. The exact timeline depends on the coordination of inspections, appraisals, and financing approvals for both properties. When selling and buying a house at the same time, professional choreography is essential to align these dates perfectly. This unhurried, steady flow ensures a stress-free experience on closing day.

What happens if my current home sale falls through after I've signed for a new house?

If your current sale falls through, your purchase contract's contingencies serve as your primary legal shield. If you have a "sale of home" contingency, you can typically withdraw from the purchase without losing your earnest money. Without this protection, you may face the financial strain of carrying two mortgages or losing your deposit. This is why expert navigation and methodical planning are critical for your long-term well-being.

Are rent-back agreements common in West Michigan real estate transactions?

Rent-back agreements are increasingly common in West Michigan, particularly in competitive areas like East Grand Rapids. These agreements allow you to remain in your sold home for 30 to 60 days after the closing date. This provides the time needed to finalize your next purchase and move directly into your new residence. It is a practical, lifestyle-oriented solution that simplifies the logistics of a dual transaction.

How do I avoid paying two mortgages at the same time?

You can avoid the burden of two mortgages by executing a simultaneous closing or negotiating a post-closing occupancy agreement. By aligning the closing dates for both properties on a single day, you ensure that the funds from your sale immediately pay off your old loan. Our concierge-level management focuses on this exact choreography. It transforms a complex logistical challenge into a seamless, supportive journey for your family.

What are the tax implications of selling and buying a house in the same year?

Most homeowners can exclude up to $250,000 in capital gains from their taxes, or $500,000 for married couples, if the property was their primary residence. When selling and buying a house at the same time, you should also monitor Michigan's real estate transfer tax. A bill to eliminate this 0.75% tax passed the Michigan House in May 2026. Consulting a tax professional ensures you understand how these shifts impact your specific evolution.