What if the mortgage amount your lender approved isn't actually the number that will allow you to thrive in your next chapter? Determining how much house can I afford in Grand Rapids MI requires looking beyond a simple loan certificate and into the specific, localized realities of the West Michigan market. It's a process of balancing your financial capacity, your lifestyle goals, and your long-term security.

We understand that the current landscape can feel complex. With interest rates for a 30-year fixed mortgage sitting near 6.5% and homes in Grand Rapids selling in just nine days, the pressure to move quickly is real. You want to secure a beautiful space in a neighborhood you love, but you also want the confidence that you aren't overextending yourself in a competitive environment. This guide provides the strategic clarity you need to move forward with certainty.

You'll discover how to navigate the significant tax differences between Ada and East Grand Rapids, understand the true impact of 2026 interest rates, and calculate the total cost of ownership. We will explore the nuances of local millage rates, neighborhood premiums, and lifestyle maintenance. By the end, you will have a clear, methodical roadmap for your next home purchase.

Key Takeaways

- Define your strategic affordability by identifying the intersection of financial boundaries, lifestyle aspirations, and long-term emotional security.

- Uncover the "hidden" cost differences between Kent County zip codes by comparing specific millage rates in East Grand Rapids, Ada, and Caledonia.

- Discover how much house can I afford in Grand Rapids MI by analyzing your debt-to-income ratio, liquid asset reserves, and 2026 market buffers.

- Navigate the complexities of buying while selling by leveraging home equity to ensure a seamless transition into your next life stage.

- Gain the confidence of a methodical roadmap through expert navigation that prioritizes your personal well-being over a simple transaction.

Beyond the Calculator: Defining Affordability in the 2026 Grand Rapids Market

Affordability is often reduced to a digital readout on a lender's screen. However, true Strategic Affordability is the intentional intersection of your financial boundaries, your daily lifestyle needs, and your long-term evolution. Asking how much house can I afford in Grand Rapids MI is the first step in a significant life transition. It requires a methodical look at more than just a monthly mortgage payment. You are not just buying a structure; you are investing in your future emotional security and personal peace.

We view home ownership as a personal milestone that marks a shift in your life story. This transition should feel seamless and supported, moving you toward a space that reflects your intentionality and goals. To achieve this, you must look beyond the standard calculators and account for the specific rhythmic patterns of the West Michigan market.

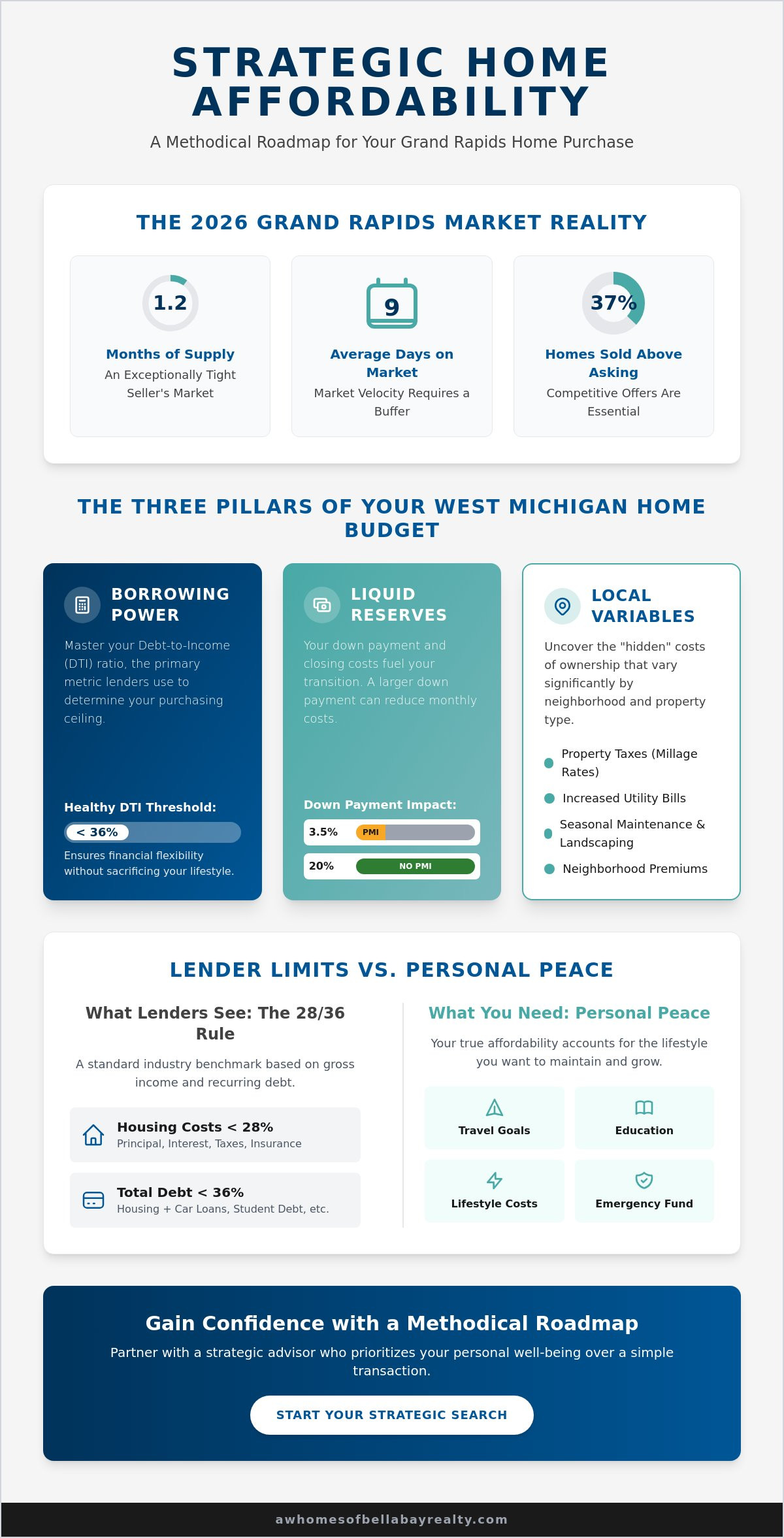

The 2026 Grand Rapids Market Reality

The current environment in Kent County remains a firm seller's market. With only 1.2 months of supply as of April 2026, inventory is exceptionally tight. Homes are going pending in an average of just nine days. This velocity means your budget needs a built-in buffer. In March 2026, nearly 37% of homes sold above the asking price. Understanding Grand Rapids, Michigan demographics and the city's steady economic growth helps explain this persistent demand. Because the market moves so quickly, partnering with a buyers agent in Grand Rapids is essential. They provide the professional authority and localized reliability needed to ensure your offer is competitive without compromising your financial safety.

Lender Limits vs. Personal Peace

Lenders typically use the 28/36 rule to determine your borrowing power. This guideline suggests that housing costs shouldn't exceed 28% of your gross income, and total debt shouldn't exceed 36%. While this is a helpful industry benchmark, it often overlooks the nuances of your personal peace. Lenders don't account for your specific travel goals, your children's extracurricular activities, or your desire for a robust emergency fund. When calculating how much house can I afford in Grand Rapids MI, you must account for hidden monthly costs. These include:

- Increased utility bills for larger square footage or older historic homes.

- Seasonal maintenance and landscaping unique to Michigan's climate.

- The gradual rise of property taxes following a sale.

A methodical approach to financial planning ensures you are buying for your future self. By setting a realistic baseline now, you protect your lifestyle comfort for years to come.

The Three Pillars of Your West Michigan Home Budget

Building a home budget requires more than a casual glance at your bank balance. It demands a structured approach that prioritizes your long-term peace. We focus on three essential pillars: borrowing power, liquid reserves, and local variables. These elements provide the structural support for a purchase that is both financially sound and emotionally secure. Asking how much house can I afford in Grand Rapids MI is a question of balance, and these pillars ensure you don't overlook the details that matter most.

Mastering the Debt-to-Income Ratio

Your Debt-to-Income (DTI) ratio is the primary metric lenders use to gauge your 2026 borrowing power. The front-end ratio compares your projected housing costs to your gross income, while the back-end ratio includes all recurring debts. Obligations such as car loans, student debt, and credit card balances can significantly reduce your purchasing ceiling. According to the U.S. Census Bureau QuickFacts, median household income in our city provides a baseline for understanding regional purchasing power. A healthy DTI for a Grand Rapids move-up buyer typically stays below 36% to ensure financial flexibility. This threshold allows you to manage your mortgage without sacrificing the lifestyle you've worked hard to build.

The Liquid Asset Requirement

Liquid assets serve as the fuel for your property transition. Many buyers explore down payment options ranging from 3.5% for FHA loans to 20% for conventional financing. A larger down payment can eliminate Private Mortgage Insurance (PMI), reducing your monthly obligation. However, you must also set aside funds for Michigan home closing costs, which cover title insurance, recording fees, and escrowed taxes. We advise clients to maintain a separate transition fund for immediate repairs or personalization projects. Having this cash reserve ensures that your first few months in a new home are defined by excitement rather than financial strain.

The final pillar is the West Michigan Variable. This includes property taxes, homeowners insurance, and seasonal utilities. Property taxes in Kent County are calculated based on millage rates that shift between jurisdictions. When determining how much house can I afford in Grand Rapids MI, you must also consider Michigan's unique insurance market and the cost of heating a home through our winter months. If you're seeking a methodical way to analyze these variables, consulting with a regional specialist can provide the clarity you need to move forward with confidence.

Neighborhood Nuances: How Location Impacts Your Buying Power

Selecting a neighborhood is a profound decision that influences your daily rhythm, your financial trajectory, and your long-term equity. In West Michigan, location is not merely a matter of proximity to downtown or the quality of the local park. It is a strategic choice that dictates the underlying math of your monthly payment. When you ask how much house can I afford in Grand Rapids MI, the answer shifts significantly as you cross township lines. We view this selection as a core component of your personal evolution, ensuring your home supports both your lifestyle aspirations and your financial health.

Millage Rates and Monthly Payments

The "hidden" cost of homeownership in Kent County often resides in the millage rates. These rates vary by municipality and school district, creating a scenario where two identical $500,000 homes can have a $400 difference in their monthly mortgage payments. For example, East Grand Rapids offers world-class amenities and a historic aesthetic, but its millage rates are among the highest in the region. Conversely, areas like Ada and Cascade often provide a different tax profile that may allow for greater purchasing power on the list price side. For deeper local insights into these tax advantages, our Ada MI neighborhood guide offers a strategic roadmap for buyers looking to maximize their budget.

The Value of Lifestyle Proximity

Beyond taxes, your buying power is impacted by the "School District Premium." High-demand districts like Forest Hills, Rockford, and Caledonia often command higher entry prices, yet they offer a consistent return on investment and stable property values. When determining how much house can I afford in Grand Rapids MI, it's vital to look at the total monthly cost rather than just the list price. This calculation should include:

- Commute times and transportation costs to major employment hubs.

- The long-term ROI of purchasing in a district with historically high demand.

- Proximity to lifestyle amenities that reduce the need for external spending.

A methodical analysis of these factors ensures that your neighborhood choice is an asset to your life story. By focusing on the total cost of ownership, you move toward a purchase that provides both emotional security and financial clarity. We believe that finding the right fit is a process of expert navigation, moving you away from chance and toward a well-planned future.

Strategic Budgeting for Move-Up Buyers and Life Transitions

The transition from one residence to another is a profound evolution of your life story. It marks a chapter of growth, intentionality, and new beginnings. For many West Michigan families, the move-up purchase is the most complex financial maneuver they will ever undertake. It requires a sophisticated balance of timing, equity, and market awareness. Determining how much house can I afford in Grand Rapids MI becomes a multidimensional calculation when you have a property to sell. We view this process as a positive development that deserves a methodical, stress-free approach.

In a market where inventory remains lean and homes go pending in just nine days, the logistics of a simultaneous buy-sell can be daunting. Strategic advisors often utilize bridge loans or specialized financing to ensure a seamless transition. These tools allow you to act quickly on your dream home without the immediate pressure of a closed sale on your current residence. This creates an atmosphere of emotional security, moving you away from the anxiety of "what if" and toward the certainty of "what's next."

Leveraging Your Current Equity

Your current home is often your most significant financial engine. Estimating your net proceeds is the foundational step in your next purchase. If you are selling your home in Forest Hills or another high-demand area, you likely possess substantial equity. A professional Comparative Market Analysis (CMA) is essential here. It moves beyond generic online estimates to provide the professional authority needed to set a realistic budget. This equity acts as a bridge, fundamentally altering the answer to how much house can I afford in Grand Rapids MI by allowing for a larger down payment, which can eliminate PMI and secure a more favorable monthly obligation.

Planning for the Next Stage

Whether you are expanding for a growing family or curating a more refined lifestyle, your budget must reflect your future needs. Move-up buyers often prioritize luxury home features such as professional-grade kitchens, smart home integration, or expansive outdoor living spaces. While these features enhance your daily rhythm, they also come with specific maintenance profiles that should be factored into your total cost of ownership. We recommend the "Five-Year Rule" for these transitions. Ensure the property aligns with your vision for at least half a decade to allow for meaningful wealth accumulation and equity growth.

To receive a personalized analysis of your current home's value and how it impacts your next purchase, request a strategic market evaluation from our expert team today.

Navigating Your Purchase with a Strategic Advisor

Determining how much house can I afford in Grand Rapids MI is a journey that requires more than a digital calculator. It demands a partner who understands that a home purchase is a significant personal milestone, not just a financial transaction. A concierge real estate approach moves beyond simple salesmanship to provide high-level consulting, emotional security, and localized reliability. By positioning your purchase within the context of your life story, we mitigate the inherent stress of the 2026 market and replace it with a structured, rhythmic path forward.

The current landscape, defined by 6.5% interest rates and exceptionally lean inventory, necessitates a methodical strategy. You deserve a professional who prioritizes your long-term well-being over a quick closing. This expert navigation ensures that every detail, from neighborhood-specific millage rates to the long-term ROI of a specific school district, is analyzed with precision. Our goal is to provide a seamless process that allows you to focus on the excitement of your personal evolution while we manage the complexities of the transaction.

The Angela Worth Advantage

AW Homes of Bellabay Realty operates with a palpable sense of strategic focus. Our property sourcing process is intentionally methodical, designed to identify homes that align with your lifestyle goals and financial boundaries. We specialize in the nuances of life transitions, providing tailored expertise for relocation clients and move-up buyers who are balancing simultaneous transactions. This approach is grounded in three essential elements: professional authority, empathetic reassurance, and expert planning. We don't just find houses; we secure the foundation for your next chapter in West Michigan.

Your Next Steps in West Michigan

Your transition toward a new home begins with a clear financial roadmap. We recommend starting with a pre-approval from a local Grand Rapids lender who understands the specific rhythmic patterns of our regional market. Following this, we can establish customized neighborhood alerts that filter listings by your strategic affordability range, ensuring you are the first to know when a property in Ada, Cascade, or East Grand Rapids becomes available. This organized approach ensures no detail is left to chance.

Defining your true buying power is a personalized process that requires expert insight. We invite you to move away from uncertainty and toward a well-planned future. Schedule your strategic home buying consultation today to discover how much house can I afford in Grand Rapids MI while maintaining the lifestyle you've worked hard to achieve.

Step into Your Next Chapter with Confidence

A home purchase is more than a financial milestone; it is a positive development in your life story. We have explored how neighborhood millage rates, lifestyle maintenance, and the strategic use of your current equity define your true purchasing power. Realizing how much house can I afford in Grand Rapids MI is a methodical process that ensures your next home is a sanctuary, not a source of stress. By balancing financial pillars with your personal evolution, you can navigate the 2026 market with absolute clarity.

AW Homes of Bellabay Realty provides expert guidance on Grand Rapids neighborhood trends and concierge-style service for move-up and relocation clients. We maintain a strategic focus on your emotional security, managing every detail to provide a seamless transition into your next life stage. Begin your strategic home search with AW Homes of Bellabay Realty today. Your future in West Michigan is waiting, and we are here to ensure your journey is supported, organized, and deeply rewarding.

Strategic Answers for Your Grand Rapids Home Purchase

What is the average home price in Grand Rapids for 2026?

The median sale price for a home in Grand Rapids reached approximately $325,000 as of April 2026. This reflects a steady upward trend, with prices increasing nearly 5% over the previous year. While this city-wide average provides a baseline, specific areas like East Grand Rapids see much higher median prices, often exceeding $738,000 due to high demand and limited inventory.

How much should I save for a down payment in the West Michigan market?

Most buyers in West Michigan aim for a down payment between 3.5% and 20% of the purchase price. While a 20% down payment eliminates the need for Private Mortgage Insurance (PMI), many successful buyers utilize FHA or conventional programs with lower entry points. We recommend maintaining a liquid reserve that covers your down payment, closing costs, and an emergency maintenance fund.

Does my credit score affect how much house I can afford in Michigan?

Your credit score is a primary factor in determining your interest rate, which directly impacts how much house can I afford in Grand Rapids MI. A higher score secures lower rates, reducing your monthly obligation and increasing your total borrowing power. For a typical $300,000 loan, even a quarter-point rate change can alter your monthly payment by $50 to $75.

Are property taxes higher in East Grand Rapids compared to Ada?

Property taxes are generally higher in East Grand Rapids due to its specific millage rates and high property valuations. Ada and Cascade townships often offer tax advantages that can provide more flexibility in your monthly budget. It is essential to compare the specific millage rates of each township to understand the "hidden" costs associated with your preferred neighborhood.

Should I get pre-approved before looking at homes in Forest Hills?

Pre-approval is an essential first step in the competitive Forest Hills market, where homes often go pending in just nine days. Sellers in high-demand areas expect buyers to demonstrate financial readiness before considering an offer. This professional documentation provides you with a clear budget, increases your negotiating authority, and ensures a more seamless transaction process.

What are the typical closing costs for a buyer in Grand Rapids?

Closing costs for buyers in Grand Rapids typically range from 2% to 5% of the home's purchase price. These fees cover professional services such as title insurance, recording fees, and the establishment of your tax escrow account. Budgeting for these costs early in the process prevents financial surprises during the final stages of your property transition.

How do I calculate my debt-to-income ratio for a mortgage?

To calculate your debt-to-income (DTI) ratio, divide your total monthly debt obligations by your gross monthly income. Lenders look at both your housing-only costs and your total debt, including car loans and credit cards. Maintaining a total DTI below 36% is a methodical way to ensure you have the financial flexibility to enjoy your new lifestyle.

Can I buy a home in Grand Rapids if I have student loan debt?

You can certainly purchase a home in Grand Rapids while managing student loan debt, provided your overall DTI ratio remains within lender guidelines. Many move-up buyers and professionals successfully balance education debt with a mortgage by utilizing strategic budgeting and equity from a previous home. We focus on your total financial health to ensure your purchase supports your long-term personal evolution.